Domenic Gallippi

Mortgage Agent Level 2 - M23007938

domenic@bettermortgagesbydom.ca

Tel: 416-801-6616 | Cell: 416-801-6616

Domenic Gallippi

Mortgage Agent Level 2 - M23007938

domenic@bettermortgagesbydom.ca

Tel: 416-801-6616 | Cell: 416-801-6616

Becoming mortgage-free is a cherished financial objective for many Canadian homeowners. By paying off your mortgage earlier than scheduled, you can save considerable amounts in interest, alleviate financial stress, enhance your financial stability and free up cash flow to do other things.

Here’s a look at some potent strategies to help you pay off your mortgage more swiftly:

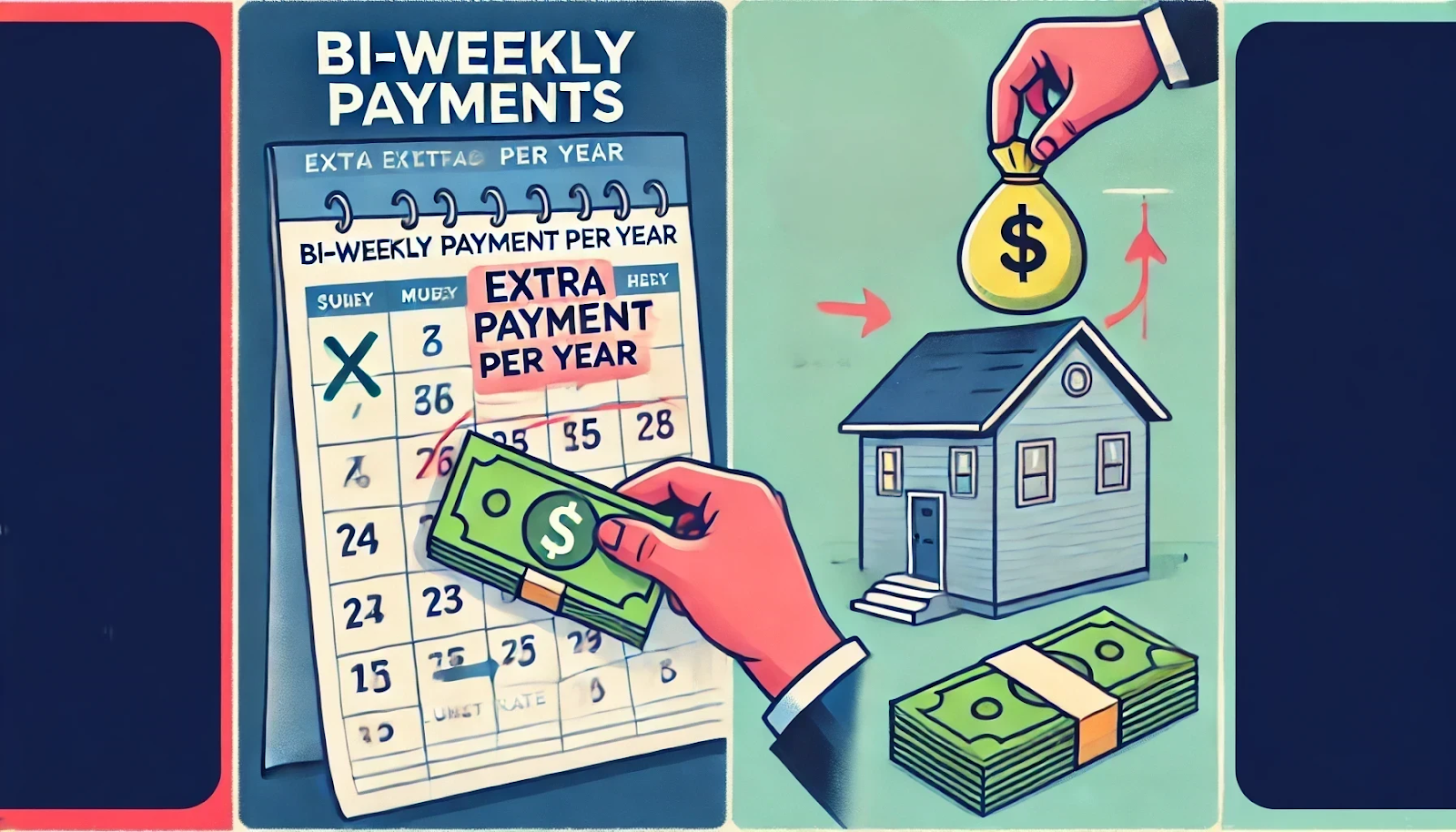

The formula for calculating accelerated bi-weekly payments is to take the monthly mortgage payment and divide it by two. With accelerated bi-weekly payments, you’ll be making the equivalent of one extra monthly payment per year. This means that by switching to accelerated bi-weekly payments, you’ll be paying off your mortgage faster and pay less interest compared to monthly payments.

A simple tweak like rounding up your payments can markedly decrease your mortgage term. Even a small increase can yield significant interest savings over time.

Applying unexpected financial gains, such as tax refunds or bonuses, to your mortgage can substantially reduce your balance. Most lenders allow lump sum payments up to 10-20% of your principal annually without penalties.

If your mortgage plan allows it, doubling your payment occasionally can drastically reduce your principal.

A higher credit score can secure you more favorable mortgage rates, reducing costs over the life of your loan. Increasing the frequency of credit card payments can help manage and possibly improve your credit utilization ratio

Refinancing if/when interest rates are lower will lower your contracted monthly payments. If you refinance, consider continuing to pay your original mortgage payment amount to reduce your principal faster.

Example: If refinancing drops your payments from $1,200 to $1,100, keep paying $1,200 to cut down your mortgage period.

It’s important to monitor interest rate trends - especially if you are in a variable rate mortgage. If rates climb and are expected to continue to climb, switching to a fixed rate might be wise. Conversely, if rates drop, you may want to lock into a fixed rate and/or maintain your higher payment amount to capitalize on the reduction.

Applying these strategies effectively requires diligent planning and consistency. Consulting a mortgage agent can be invaluable—they can guide you through the diverse products and terms available and help identify opportunities tailored to expedite your journey to becoming mortgage-free. Remember, some lenders offer more advantageous or flexible options than others, potentially aiding you in clearing your mortgage faster.

Ready to discuss your home ownership goals and a Better Mortgage by Dom?

Call/text: 416 801-6616. Email: Domenic@BetterMortgagesByDom.ca

Connect/Follow me: Facebook, Instagram, X (formerly Twitter), LinkedIn

Download my app - featuring premium interactive tools, calculators, and illustrators for smart planning and real-time rate updates

Please share with anyone that you think can benefit from my help - all introductions are greatly appreciated!